Traffic tickets can significantly impact your insurance rates, with the duration of their effects varying based on several factors. In the article How Long Does A Traffic Ticket Affect Your Insurance?, we explore how long traffic tickets remain on your record, typically between three to five years. The increase in insurance rates also depends on the severity of the offense; more serious violations can lead to steeper hikes in premiums. Additionally, the article provides actionable tips to minimize the financial impact after receiving a ticket, such as attending defensive driving courses or maintaining a clean driving record post-ticket. Understanding the interplay between traffic violations and insurance is crucial for drivers looking to manage their costs effectively. This comprehensive guide equips readers with the necessary knowledge to navigate their insurance landscape after a ticket.

Understanding The Impact Of Traffic Tickets On Insurance Rates

When you receive a traffic ticket, the impact on your insurance can be significant and long-lasting. The question many drivers have is How Long will this impact last? Generally, a traffic violation can cause your insurance rates to increase for three to five years. The extent of this increase may depend on various factors, including the severity of the violation and your driving history. Understanding these dynamics can help you navigate the potential financial consequences of a traffic ticket.

Different types of tickets also influence insurance rates in varying degrees. For instance, a speeding ticket might result in a mild increase, while more serious offenses like DUIs can cause far greater hikes. Evaluating your specific situation with your insurance provider can give you tailored information about how How Long your rates will be affected by each type of violation. Moreover, some states have specific laws governing how points impact insurance, further complicating the picture for drivers.

| Type of Violation | Typical Insurance Rate Increase | Duration of Impact |

|---|---|---|

| Speeding Ticket | 10%-20% | 3-5 Years |

| Reckless Driving | 20%-40% | 3-5 Years |

| DUI | 30%-100% | 5-10 Years |

There are various key factors that determine how traffic violations influence your insurance rates. Understanding these factors can help you better predict and manage any potential increases after receiving a ticket. Here are some components you should consider:

- Key Factors Influencing Insurance Rates

- Type of violation: Different violations incur different impacts.

- Your driving history: A clean record may lessen the penalty.

- Insurance provider policies: Each insurer has its own guidelines.

- State regulations: Some states have stricter laws regarding traffic violations.

- Duration of the violation on record: Points may affect rates for several years.

Ultimately, traffic tickets not only serve as legal penalties but also impact your financial stability through increased insurance premiums. Being informed about How Long your rates might be affected can empower you to make better decisions on the road, as well as in managing your insurance policy. Knowing your rights and seeking advice from insurance professionals can also help mitigate the effects of any future tickets.

How Long Does A Traffic Ticket Stay On Your Record?

The duration a traffic ticket stays on your record can significantly impact your insurance rates. Generally, how long a ticket affects your insurance depends on various factors, including the severity of the offense and your state laws. In many cases, minor infractions may remain on your record for 3 to 5 years, while more severe violations can linger for up to 10 years or more. Understanding this timeline is crucial for drivers to anticipate potential rate increases and make informed decisions regarding their insurance coverage.

| Type of Violation | Duration on Record (Years) | Typical Insurance Impact |

|---|---|---|

| Minor Traffic Violations | 3 | Moderate Increase |

| Major Traffic Violations | 5-10 | Significant Increase |

| DUI or Reckless Driving | 7-10 | Severe Increase |

When considering the effect of a traffic ticket on your insurance premiums, it’s essential to recognize the implications of different types of violations. Insurance companies often assess the risk level associated with a driver’s record when calculating rates. For instance, a simple speeding ticket may only lead to a temporary increase in rates, while a DUI could result in long-term consequences that affect your insurability. The longer a ticket stays on your record, the greater the chance it will play a role in your insurance calculation.

Steps To Check Your Driving Record

- Visit your state’s Department of Motor Vehicles (DMV) website.

- Locate the section for requesting your driving record.

- Fill out any required forms online or in-person.

- Provide your personal information for verification.

- Pay any applicable fees to obtain your record.

- Review your driving history for any inaccuracies.

- Request corrections if necessary.

Ultimately, awareness of how long a traffic ticket remains on your record allows drivers to take proactive measures in managing their insurance costs. Regularly checking your driving record can help you stay informed and address any discrepancies that may lead to higher premiums. Moreover, by understanding the link between driving infractions and insurance rates, drivers can strategize their actions to keep themselves safe on the road and minimize unnecessary financial burdens.

Factors Affecting The Duration Of Insurance Increases After A Ticket

Understanding the implications of traffic tickets on your insurance rates involves various factors. One significant aspect to consider is the severity of the offense. Minor infractions, such as rolling a stop sign, may impact your insurance for a shorter period compared to more serious violations like DUIs or reckless driving. Insurers typically review your driving history and categorize offenses to determine how long your insurance will be affected. Thus, it is essential to appreciate that not all tickets carry the same weight.

| Ticket Type | Typical Duration of Insurance Increase | Severity Level |

|---|---|---|

| Speeding | 3 years | Moderate |

| Running a Red Light | 3 years | Moderate |

| Reckless Driving | 5 years | Severe |

| Driving Under the Influence (DUI) | 7 years | Severe |

Another factor influencing how long your insurance costs may increase is the type of insurance policy you have. Premiums can vary widely from one provider to another, and some may be more forgiving than others when it comes to adjusting rates after a ticket. It is crucial to understand your specific policy’s terms and how different insurance companies assess risk. This understanding can play a significant role in navigating the aftermath of receiving a traffic ticket.

Situations That May Affect Insurance Rates

- Accumulation of multiple tickets in a short period

- Driving experience and history

- Type of vehicle being insured

- Insurance company policies and underwriting criteria

- Location and traffic conditions in your area

- Completion of traffic school or defensive driving courses

Additionally, your continuous driving behavior post-ticket can also influence how long the increased rates linger. If you maintain a clean driving record following the ticket, insurers may consider you a lower risk over time. Conversely, further infractions during the penalty period may lead to longer-lasting impacts on your insurance rates. In summary, a combination of factors determines how long how long you may face increased insurance premiums after receiving a traffic ticket, making it vital to remain aware of your driving habits and policy specifics.

Comparing Insurance Rate Increases By Ticket Type

When it comes to understanding how long a traffic ticket affects your insurance rates, it’s crucial to consider the type of violation. Different offenses can lead to varying impacts on your insurance premium due to their severity and risk associated. Some minor infractions might result in slight increases, while major violations can significantly spike your rates. Therefore, categorizing tickets can help in estimating the potential insurance consequences more accurately.

Here are some common ticket types and their potential effects on insurance rates:

| Ticket Type | Typical Rate Increase | Duration of Impact |

|---|---|---|

| Speeding | 20-30% | 3-5 years |

| Running a red light | 25-35% | 3-5 years |

| Driving under the influence (DUI) | 50-100% | 5-10 years |

| Failure to stop | 15-25% | 3-5 years |

As illustrated in the table, a driving under the influence (DUI) charge has the most severe impact on insurance rates, with increases potentially reaching 100% or more. In comparison, less severe tickets, such as a minor speeding violation, could result in a more modest increase. This emphasizes the importance of understanding the specific violations and their long-term implications on your insurance costs.

Ultimately, the duration of a ticket’s effect on your premium will vary based on several factors including state laws, the severity of the offense, and your individual driving history. Insurers may also have different policies regarding how they treat specific tickets. A careful examination of these factors can help you better anticipate the overall effects of a ticket on your insurance and plan accordingly. In summary, knowing how long these increases might last can lead to informed decisions regarding your driving habits and insurance choices.

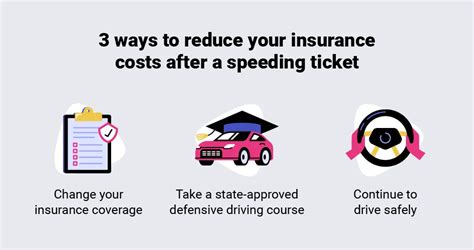

Actionable Tips To Minimize Insurance Impact After A Ticket

Receiving a traffic ticket can be a stressful experience, especially when considering the potential impact on your insurance premiums. It’s crucial to understand how long these effects can last and what actions you can take to mitigate them. While the length of time a ticket stays on your record and influences your rates may vary, how long your insurance premiums are affected is often customizable through proactive steps.

To begin minimizing the insurance impact after a ticket, you may want to consider enrolling in a defensive driving course. Many states offer these programs, which could not only help lower your risk profile but may also allow you to qualify for discounts on your insurance premiums. Additionally, consistently maintaining a clean driving record post-ticket can signal to insurers that the incident was an anomaly rather than a pattern of risky behavior.

| Tip | Potential Impact Reduction | Timeframe for Effect |

|---|---|---|

| Complete Defensive Driving Course | Up to 10% | Immediate to 3 years |

| Maintain Clean Driving Record | Varies – Typically 20% | 3-5 years |

| Shop Around for Insurance | Variable | Immediate |

| Increase Deductibles | Potentially lower premiums | Immediate |

Another key action is to review your insurance policy and shop around for better rates. Different companies weigh tickets differently, which means that you might find more favorable options elsewhere. Additionally, increasing your deductibles can lead to lower monthly premiums and help in absorbing the financial impact of insurance rate increases due to a traffic violation.

Steps To Take After Receiving A Ticket

- Assess the ticket and understand the specific violation.

- Consider attending a defensive driving course.

- Contact your insurance provider to discuss policy implications.

- Review and compare different insurance options.

- Maintain a clean driving record moving forward.

- Inquire about available discounts or lower-risk options with your insurer.

- Consider seeking legal advice if the ticket has severe implications.

In conclusion, it’s essential to take proactive measures if you’ve received a traffic ticket. By understanding how long it may impact your insurance and implementing effective strategies to minimize its effects, you can protect your financial interests and potentially lower your insurance costs moving forward.